Once upon a time, financially responsible Americans looked forward to their Golden Years.

After years of saving money, retirement meant carefree time to spend with family and friends, enjoy hobbies, or travel the world.

But now, according to a startling survey by Allianz Life Insurance, “a remarkable 64% of Americans say they are more afraid of running out of money than they are of death.”

And they have no specific financial plans in place to avoid seeing their worst fears come true.

It’s a psychological sign of these uncertain times.

It’s also an unsettling indicator of just how challenging preparing for a stable financial future has become.

After witnessing so much economic turbulence sweep the nation over the last decade, many baby boomers (61–79 years old) find themselves concerned about America’s economic future.

But boomers aren’t the only generation feeling the pinch…

According to the Allianz survey, Gen Xers (45–60 years old) and Millennials (29–44 years old) are even more anxious than older folks.

Gen Xers would be concerned with their income levels not growing fast enough to keep up with the rising costs of living and not having saved enough to retire.

Millennials, on the other hand, still have “plenty of time” to save and prepare. But like the Gen Xers, many may not be able to save enough to keep up with the costs of inflation. And many have no plan in place to protect what wealth they do manage to set aside.

Regardless of age, income, or experience, the Allianz survey results show…

Almost 40% of Americans admit their retirement strategy is getting out of hand as “they are not saving as much for retirement as they would like.”

What’s the problem?

The study cites “inflation, taxes, market volatility, financial crises, and other challenges.”

And to make matters more challenging, 54% of Americans only have a basic 401(k) or IRA. Which leaves them vulnerable to inevitable market turbulence and its effects on their accounts’ long-term performance.

Even fewer have taken deliberate, planned steps to help protect their wealth from future economic uncertainties.

But the day-to-day needs are so pressing for many people that they’re not focusing on their financial future… Instead, it’s all about getting by in the near term: according to the Allianz survey, a whopping 63% of Americans cite rising daily expenses as the most common factor keeping them from saving for retirement.

This is understandable.

But it’s important to plan ahead because…

America’s future includes possible economic challenges that may make saving and retirement planning that much more difficult.

For example, the value of the US dollar:

Most people aren’t aware just how far the purchasing power of their dollars has dropped or how fast it’s fading away.

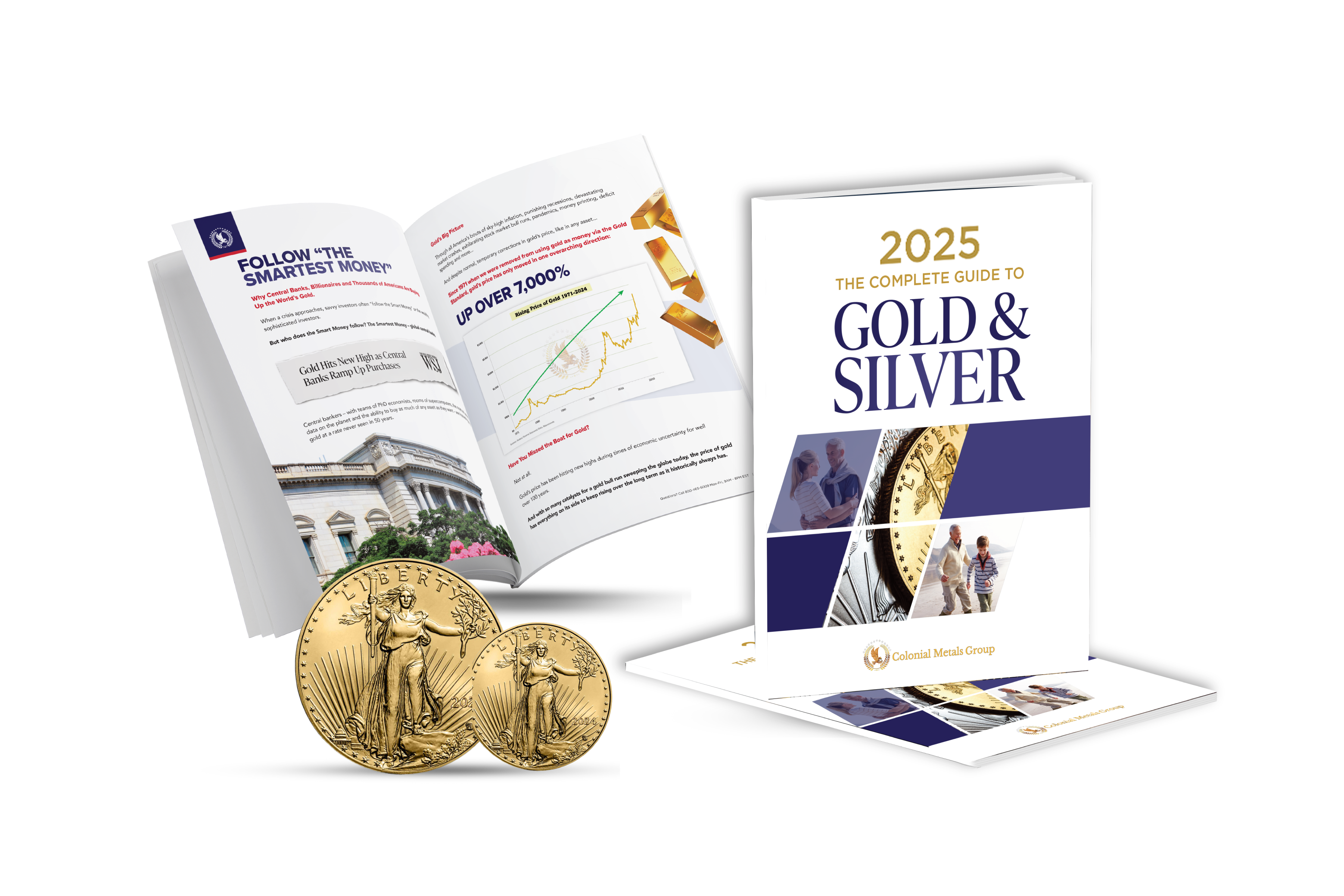

Every dollar you saved since 2000 has lost 47% of its value…

And as the government continues to borrow, print, and spend, devaluation will only increase which means that the basic costs of living will go higher in dollar terms.

This means relying solely on savings to cover future living expenses may be problematic.

But what about Social Security—the government fund in place to take care of older Americans who “paid their financial dues” over the years?

Well, according to The Brookings Institution, Social Security is in big trouble.

Because official data shows the Old-Age and Survivor Insurance (OASI) Trust Fund—the source of the program’s retirement benefits—is forecast to exhaust its funds in 2033. And unless the government steps in to fix the fund, annual benefits will be slashed by 17% or more for retirees.

All of this taken together paints a tough future for the unprepared.

Especially since we are living longer. And the longer we live, the higher the statistical probability of a major personal health crisis, increased geopolitical turmoil, more lost purchasing power, and economic crises.

“With Americans living longer in retirement and facing risks like market volatility, creating a financial strategy so that your money lasts your lifetime is a daunting task. A strong retirement strategy will go beyond a dollar amount in the bank,” says Allianz’s Kelly LaVigne.

We here at Colonial Metals agree. And we believe an important part of that proper planning includes protecting your wealth with gold—before the inevitabilities of a debt-laden economy affect your financial future.

But perhaps more importantly, from the very personal mental state of someone who owns gold, gold’s greatest value is its ability to help alleviate fears of running out of money before you run out of years.

And for anyone near retirement or just beginning to enjoy their Golden Years, that kind of financial peace of mind is priceless.

Please don’t hesitate to reach out to us with any questions you may have.

May you be safe and well during these uncertain times.

Todd Sawyer, Director of Client Education

Colonial Metals Group